As announced during Budget 2024, the federal government is ready to extend the service tax from the 6% rate at present to eight% as of March 1. There are just a few categories which can be excluded from the brand new rate, including F&B and telecommunications, but on the whole, consumers are set to pay more in consequence of the hike.

It has already been indicated that vehicle servicing and repairs don’t fall under exempted categories under the revision, and so vehicle maintenance is ready to cost more from March 1. Keep in mind that the service tax on this case is barely applied to labour charges and never on the parts themselves.

In any case, the fun doesn’t really end there, because one other area where motorists are set to pay more is motor insurance. Nothing has really been highlighted about this within the news up to now, however the segment will certainly see the two% increase being applied on it, as all business-to-consumer general insurance or takaful, excluding medical insurance or medical takaful is subject to service tax.

Will it cost you significantly more? Well, not quite, even though it depends upon the coverage or slightly how much you really must fork out for the premium itself. The service tax for motor insurance is charged on the actual premium paid, which suggests it’s calculated on the sum after NCD, if any, is applied.

Taking the resident Honda CR-V’s 2023 insured sum of RM96,200 for example, the service tax is RM102.84 on a premium costing RM1,713.97 (after applying 55% NCD). That’s at 6%, and should you apply an 8% rate on the premium to get a gauge of how things shape up, the service tax could be RM137.12, which is an additional RM34.27.

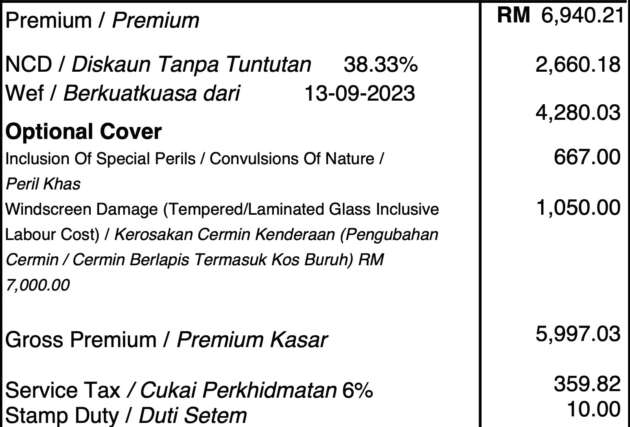

One other example is provided by Hafriz’s Range Rover Sport, for which he presently pays RM5,997 (with 38.33% NCD applied) in insurance. The service tax for that’s RM359.82, and this may increase to RM479.77 if calculated with an 8% rate, translating to an extra RM119.95.

Because it is with servicing costs, the margin of increase from a standalone viewpoint isn’t drastic (unless labour charges are exorbitant and the vehicle you’re insuring is well, expensive), but like with the rise within the electricity tariff for consumers who use between 601 kWh and 1,500 kWh a month, it represents additional, unavoidable spend, and it would add up.

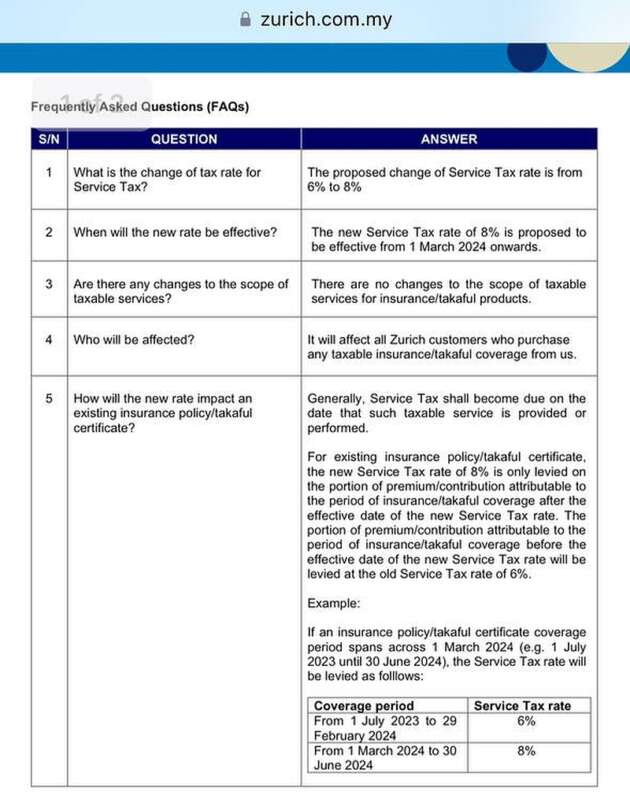

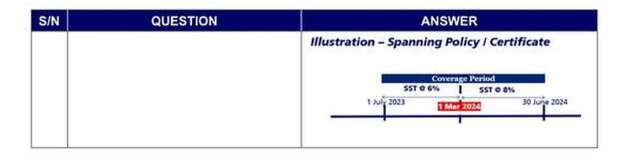

Regarding the appliance of the brand new service tax rate, here’s an interesting bit – consumers may very well must pay more for his or her existing motor insurance if coverage runs through March 1, if that in an FAQ by Zurich Malaysia is correct.

The FAQ notes that the tax will probably be applied partially on existing policies, where a policy with a coverage period from July 2023 to June 2024 will see the duration of coverage from March 1 to the tip of the coverage period in June being subject to the service tax increase.

It will not be known whether it’s blanket across all providers, however it it looking more likely to be the case, as an MSIG post on its Facebook page notes the rise within the service tax in addition to the next commentary:

“MSIG reserves the proper to gather any undercharged service tax for policies processed before 1 March 2024 where the insurance period spans across 1 March 2024. You’re obligated to pay any applicable taxes including but not limited to service tax and stamp duty which can be imposed by the Malaysian tax authorities in relation to your policy.”

Should this be the case, the query could be, while the calculation will probably be pro-rated, how exactly will policy holders pay for the adjustment? We’ve reached out to PIAM to search out out more about this, and can update once we get further information.

Seeking to sell your automobile? Sell it with myTukar.

This Article First Appeared At paultan.org